The Boom and the error of optimism give way to a crisis of confidence and fear, the error of pessimism...

The most pertinent question which is

asked recently is the fact that whether we are in the preliminary stage of a

bull market and whether the economic cycle is turning around for good in India? There

are no easy answers as far as the timing of the bull market is concerned. From

a generalized standpoint, we know for sure that there are four stages as far as

sentiment goes i.e., optimism, euphoria, pessimism and depression and from

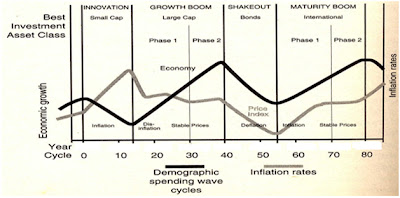

economic cycle perspective it’s innovation, growth boom, shakeout and maturity

boom and for stock market cycles there are six phases which we have discussed

in details.

For business cycles and stock markets

the most alluring part is that there is always life after death. A new cycle

always emerges as if a reincarnation, with newer set of stocks and principles

and it always tends to be different from the earlier ones. The only constant in

the nature is “Change” and the constant changes which we see or observe over

electronic media and travelling in different cities and states and countries gives

an impression of the state of economic prosperity we are in, and its

culmination into stock markets.

Likewise we have tried to put emphasis

on events and symptoms of varying degrees in order to identify the lifecycle

and stages of emerging markets. The more extreme the market peculiarities, the

more easier it becomes to identify the phase of cycle the stock market is moving

into. We have tried to put things in context and have also taken extracts from

Marc Faber’s book, where the phases have been well articulated.

Phase Zero- After Crash

- Long-lasting economic stagnation or slow contraction in real terms

- Real per-capita incomes go flat or have been falling for some years

- High unemployement

- Little capital spending and international competitive position deteriorates

- Political and social conditions become unstable(strikes, high inflation, continuous devaluations, terrorism, border conflicts, etc)

- Capital flight

Phase One- The Spark

- Social, political and economic conditions begin to improve(new government, peace treaties, adoption of market economies and capitalistic systems, introduction of property rights, etc)

- New economic policies(tax cuts and preferential treatment of foreign direct investments, removal of capital gain taxes, currency reforms, lifting of foreign exchange controls, permission for foreigners to acquire 100% of assets including real estate, removal of trade barriers, etc)

- External factors, discoveries of resource deposits, the rise in price of an important commodity, applications of new inventions and innovations

- Improvement in liquidity because of an increase in exports, the repatriation of capital and increasing foreign portfolio flows and direct investments

- The outlook of future profit opportunities improves significantly, as a result of one or several above mentioned factors

- The undertaking of large scale infrastructure projects that improve power supplies, road transportation and port facilities

- The privatization of entire industries

Phase Two- The Recovery Cycle

- Unemployement falls and wages rise

- Capital spending to expand capacity soars, as the improvement in economic condition is expected to last forever(error of optimism)

- Large inflows of foreign funds propel stocks to overvaluation

- Credit expands rapidly, leading to a sharp rise in real and financial assets

- Real estate prices increase several fold

- New issues of stocks and bonds reach peak levels

- Foreign brokers and other foreign financial institutions open offices

- Merger and acquisition activity picks up

- Inflation accelerates and interest rates begin to rise

- There are exceptions, however: When countries suffer from hyper inflation and depression at the same time, the recovery, which is usually brought about by a financial reform, will lead to declining inflation and interest rates.

Phase Three: The Boom

- Overinvestment leads to excess capacity in several sectors of the economy

- Infrastructural problems, bottlenecks and an excessive credit expansion lead at times, via rising wages and real estate prices, to strong inflationary pressures

- The inflationary pressures, however, may not take place for consumer prices

- The rate of corporate profit growth slows, and in some industries it begins to fall

- Usually, but not always, a shock such as sharp rise in interest rates, massive fraud, a business failure, margin call that cannot be met by a large speculator or some external unfavorable event leads to sudden and totally unexpected decline in stock prices

- At times stock prices decline for no other reason than that they have run far ahead of themselves, and some speculators or insiders – in the know that the boom cannot go on forever and seeing that the profit picture is deteriorating – decide to take profit

- In such cases, it is simply a matter that at some point the supply of equities from the corporate sector and insiders exceeds the demand from the stupid and credulous public who, brainwashed by the bullish statements from the corporate executives and the press, continue to buy at any price

Phase Four – Downcycle Doubts

- Credit growth slows – unless monetary authorities act irresponsibly and attempt to prolong the mania and keep the economy in a state of permanent boom

- Corporate profits deteriorate

- Excess capacity becomes a problem in a few industries, but overall the economy continues to do well and the slowdown is perceived to be only temporary

- After a initial sharp fall, stocks recover as foreign investors who missed stock markets rise in phases on and two pour money into the market and as interest rates begin to fall

- It is not uncommon that foreigners increase their buying of stocks in phase four, since they tend to be latecomers to the investment party

- Some sort of major hook keeps investor interest in the market alive. They hook may be an economy that continues to grow, sharply declining interest rates, corporate profit that are still rising, or simply optimistic statements by business leaders and government officials

- The majority of stocks usually fail to reach a new high because a large number of new issue meet demand( the sellers who are mostly locals who either know better or are strapped for cash)

- However, it is possible that a stock market index driven by just few stocks makes a new high. The advance/decline line and the number of stocks hitting new all time highs will, in such case, not confirm the new high

Phase Five – Realization

- Credit becomes tight, bond spreads widen considerably and bankruptcies soar

- Economic, but even more so social and political, conditions now deteriorate badly. Consumption slows noticeably or falls (car, housing and appliance sales are down)

- Corporate profits collapse

- Stocks enter a prolonged and severe downtrend and foreigners begin to exit

- Real estate prices fall sharply

- One or several big players go bankrupt (usually the ones who made the headline in phase three)

- Companies are strapped for cash and are often forced to issue shares at distressed prices. This increase the supply of shares and depresses prices even further

Phase Six – Capitulation and the

Bottom

- Investors give up on stocks. Volume is down significantly from the peak levels reached in phase three – usually by 90%

- Capital spending falls sharply (error of pessimism)

- Interest rates decline further and reach their lows for the cycle

- Foreign investors lose appetite for new investment and continue to sell

- Rating agencies threaten to downgrade the country

- The currency is weakening or is devalued

It

is not necessary that all the events matches in a picture perfect style in all

the stages and we shouldn't become too dogmatic about it. Generally Phase-Three is the most noticeable one and can be easily

identified. It’s in phase three that we see once in a decade kind of mania and

market completely losing its actual fundamental touch. Money making becomes extremely

easy and quick bucks are made with huge volumes and intense momentum. Symptoms

generally remains abound with

- Business capital and metro cities resembles a boom town- nightclubs packed with speculators and brokers who made handsome money in the stock market

- Volume of credit expansion explodes in the system and leverages play a greater role

- Corporate tend to make fairly large acquisition with leverages both overseas and domestic at exorbitant valuations

- Buzzwords such as LBO’s, M&A, PE fund, Venture Capital, Rising India, Superpower are used frequently. Speculator tends to remember only the script code rather than the company name

- FII flows hits a crescendo with buzzword like the ETF money, Hedge Funds etc., etc., becomes rampant

- People generally argues for a structural bull market with lofty index and stock targets and gives arguments why the stock market or the property market cannot go down

- New airports are planned for and SEZ, new cities, new industrial zones are planned and developed for. Tall and lavish buildings are constructed.

- Housewives become active in the stock market. People tend to give up full time jobs in order to concentrate playing the markets. New breed of young investors tend to perform better than the seasoned money managers and talks about winning stock market formulas

Generally

in this phase even after a sharp decline and major shock, the mood remains

optimistic and they tend to buy on decline. Capital loss in first decline is

not serious and thereafter further declines put systemic strains and serious

havoc among varied class of investors and speculators

Phase

four starts thereafter with financial strains. Leveraged speculators are forced

to sell. Lending standards are tightened and bad loans begin to climb. Tourist

arrivals slow and hotel occupancy rate declines. Brokers continue to publish

the most bullish reports arguing of a life time opportunity. Finally political

and social conditions deteriorate. The recovery in the phase four happens with

selected stocks and sectors, taking the indices higher closer to all time highs

or may even conquer it with thin volumes and narrow advance/decline ratio. The

powerful recovery generally tends to seduce investors and speculators. Economy

continues to do well after a brief pause and corporate continues to post profit

growth though the intensity and pace declines significantly.

The

transition from phase four to phase five is passive with no major knee jerk

reaction. Rather a drifting lower kind of market with symptoms’ such as falling

GDP, unfinished construction sites, higher budget deficits, stock brokers laying

off staffs or even close down and research reports becoming thinner. Country no

longer remains a favorite tourist destination. People generally tend to realize

their follies and give up on stocks and any rallies are perceived as an

opportunity to sell at the end of phase five rallies and in the phase six.

Phase

six becomes the actual climatic phase where interest rate is perceived to hit

trough. Negative headlines rules the media, currency weakens considerably on

current account imbalances and fiscal deficit burgeoning. Flights, hotels and

nightclubs are empty, foreign brokers turns bearish and shut shops. Volumes

decline sharply and mutual funds corpus decline with persistent outflows. Post

a panic selling or a capitulation on depressed economic and political

environment, stock price reaches historical low valuation and negative news

doesn’t affect the prices much and hence prices no longer declines and start

building base for a next wave of bull market.

The

Boom and the error of optimism give way to a crisis of confidence and fear, the

error of pessimism.

Identifying the Climatic Phase

As

far as Indian market goes, it’s clearly evident from the symptoms in 2006 and

2007, that final run-up to 6300 in Nifty was a phase three phenomenon where

money making was quick, volumes were huge and sentiment run euphoric. Thereafter

with the massive fall and the bubble burst, led us to phase four with fewer stocks reclaiming

their all time highs by 2010 and indices almost retesting it’s life high. After

phase four with market almost kissing 6300 in Nifty, phase five culminates in

2011 with the whole year seeing a worsening of sentiment with scams, slowdown

in the economy, interest rates reversing its trend and starts declining, brokers

laying off big time and many foreign brokers shutting shop. Phase six generally

coincides with further worsening of sentiment and capitulation. Phase five and

six are quite tricky in a sense that when phase five converts into phase six is

difficult to identify. Phase six generally is the mirror image of phase three.

Generally in phase five brokers lay off employees, leveraged companies resort to fire

sale of their assets and depress share prices further, corporate profit

deteriorates as had been seen in 2011 and in phase six currency weaknesses

reaches a climatic stage, interest rates hits a trough. At present with a

series of reforms in India, INR has reversed its trend after hitting 57.32 but

interest rates still not hitting trough with repo hovering at 8 %( last

registered trough was at 4.75%). Phase six till now has not been clearly

evident and a capitulation haven’t happened in any meaningful way and complete.

Though the confusing part is that stock specific capitulation has happened and

in dollar terms index have declined 40% in 2011. Moreover Political chaos

generally continues in phase zero and currency continues to remain weak in this

phase with high inflation. So clearly one can construe that we may be meddling

between phase six and phase zero and we can conclude the ending of phase six

once the interest rate declining cycle gathers momentum and come closer to the troughs

and valuation starts looking cheap…

Longterm

Economic Cycles with Four phases- Innovation, Growth Boom, Shakeout &

Maturity Boom along with demographic spending wave cycles and preference of

investment class at different phases

Paras Bothra

paras.bothra@ymail.com

+91 9831070777