Japan goes back to bigger quantitative

easing; American recovery quickens; European and Chinese inflation also lower

and more stable. Competitiveness

concerns may finally force RBI’s hand to lower rates.

In the weekend

before Christmas, as the world’s financial markets sauntered into holiday-hibernation,

Shinzo Abe - Japan’s Prime Minister-Elect - bettered Santa Claus (or Attila the

Hun, depending on your perspective) by declaring that his coalition, which

holds an unassailable two-thirds majority in the lower house of the Japanese

Parliament, may change the law governing the coy Bank of Japan (BOJ) if it

refuses to accept a 2 per cent inflation target at its January meeting. In any

case, Masaaki Shirakawa, the relatively hawkish BOJ governor will be replaced

with a more dovish, pliable candidate by April 2013. At the December 20th meet,

he already declared to engage in more easing by expanding asset-buying and

lending program by a tenth to $1.2 trillion, and hinted at an upward review of

its 1 percent inflation target.

Japan following Europe in moving from

inflation targeting to dual targeting

The BOJ, like

the European Central Bank (ECB), is at least in theory an inflation-targeting

central bank but Abe wants it to have a dual target of inflation and employment

much like its American counterpart - the Federal Reserve (“Fed”). But a year

ago, of course, the ECB had de facto reneged

on or at least expanded its inflation-targeting mandate by launching its first

series of Long Term Refinancing Operations (LTRO) with 489 billion

freshly-created Euros, the full (bullish) effects of which took months to play

out. The Fed of course must itself be confused about its Quantitative Easing

(QE, a term first used in Japan) historiography, with its even larger and

multifarious rounds since late 2008 or early 2009 (depending on how QE is

defined).

Yet, Japan

has no real short-term alternative policy plan given its political economy.

October 2012 figures show that CPI or consumer price inflation was negative

0.4% (or deflation), inflation has been largely negative or zero for the last

few years and nominal interest rates cannot really go down any more. Differences

on monetary easing therefore is on the margins, and imaginative solutions are

politically locked as of now – immigrants a.k.a new tax payers are still

frowned upon, an aging population creates more fiscal dependents, free trade in

agriculture is taboo, and finally there is no political force that can resist

the asymmetrical Keynesian orthodoxy in Japan. “Bridges to nowhere” are still

being touted as an economic solution, whereas structural supply-side reforms

and targeted growth-supporting tax cuts are relatively frowned upon.

All this

combined with even slower growth rates since the financial crisis of 2008 has

ballooned Japan’s government debt to GDP ratio from 167% in 2008 to 212% in

2012. Yes, interest rates have fallen since 2008 and the flow of debt servicing

has been easier to manage. But this huge stock of debt will still be around,

when – not if – interest rates rise. Yes, even China’s economic size at market

exchange rates (as opposed to purchasing power parity rates which are more

favorable to poor per-capita countries like India and China) has now clearly

overtaken Japan’s and is almost half of America’s size, yet the Government of

Japan’s debt at around 12 trillion USD is comparable to the US Government’s 15

trillion (whereas the American economy is almost three times as large as

Japan’s).

The Yen depreciates, re-establishing

itself as a carry trade generator?

Moreover, the

situation is not radically different in the US or EU, and easing there – along

with the continuing slowdown - had forced the Yen up and weakened Japanese

exports (Japan posted a larger-than-expected trade deficit in November). While

a few large countries or economic blocks could sit together and theoretically

stop down competitive devaluation, this is unlikely to happen because

democratic governments come to appreciate seigniorage and inflation as hidden

taxes that also re-adjust the balance between labour and capital in favour of

the latter without having to force the former into nominal wage cuts.

Already, the

Yen has depreciated from 79.5 in mid-November 2012 to above 84 before Christmas

in anticipation of Abe’s victory and policies. That is a 5 percent short-term

competitive advantage for Japanese exporters and manufacturers and will help at

the margins. Such overall Yen structural

weakness might mean borrowing in yen and investing in foreign currencies, which

might be a boom for Indian and other emerging market (EM) equities, if not

commodities (where supply-side booms and demand-side drops due to technical

innovations continues apace)

Jump off fiscal cliffs or not,

American central bankers will still ease for now.

The current

fight over the “fiscal cliff” in the United States exemplifies the inability of

the political class the world over to lead its societies to defer more

consumption and gratification for the well being of their children and

grandchildren. American Democrats would not countenance any stricter criteria

for redistribution payments, and many congressional Republicans would not accept

any higher taxes on upper-middle class families. Ben Bernanke’s Fed, blessed

with America’s size and credit history, is in a unique position to further ease

and yet attract lower yields with every economic downturn (including a fiscal

tightening), despite the total government to debt ratio having breached 100%.

But signs of American solvency – any ratings downgrade hysteria notwithstanding

– are inaccurate and overly pessimistic: US GDP increased at an annualized

inflation-adjusted rate of 3.1 percent in the third quarter of 2012 (that is,

from the second quarter to the third quarter). In the second quarter on the

other hand, GDP had increased by “only” 1.3 percent –strengthening the recovery

thesis. The Consumer Price Index for All Urban Consumers (CPI-U) declined 0.3

percent in November on a seasonally adjusted basis, hinting at perhaps more room

for easing at least in the short run. Over the last year, the overall price

index increased by just 1.8 percent.

The Fed therefore

said it will buy $45 billion a month of Treasuries (and 40 billion additional

dollars worth of mortgage securities) starting in January, expanding its

asset-purchase program indefinitely until 6.5% unemployment is not reached, and

so long as inflationary expectations one to two years in the future does not

breach 2.5%. Total nonfarm payroll employment rose by 146,000 in November, and

the unemployment rate went down to 7.7 percent. An additional drop of 1.2

percentage points in official unemployment rates will take at least two more

years by current estimates. But why is all this easing not leading to inflation

(yet)?

As the

financial economist Dr. Scott Grannis writes, the US public holds $6.5 trillion

of bank savings deposits (up 64% in the past four years) paying almost nothing

– 1.5 trillion of those could be diverted (as they are excess bank reserves) to

entrepreneurial activities or consumption. Therefore, while the monetary base

has exploded in recent years the M2 measure of money supply in the United

States has grown only slightly faster than its long-term average of 6%,

partially because the public does not see that many organic or structural

investment opportunities.

Moreover, the

American economy (and more specifically the housing market) continues to

“optimally” strengthen, as Ray Dalio of Bridgewater Capital might say - because

of moderate monetary policy led-leveraging (mortgage refinancing help, and

demographic expansion) with fiscal policy and private sector partial

deleveraging. 2011’s brisk revival was continued this year, with a 22 percent

increase in housing starts in the last 12 months.

Whither Europe?

Just like

politicians from India to US have not had the courage to pass many genuinely

short-term austerity and long-term liberalization measures, Mario Draghi’s ECB has

nudged Germany to repeatedly cave in to the demands of smaller, profligate countries

like Greece which refuse to fully accept painful restructuring.

The European

fiscal union – and indeed the single European nation-state – is being molded

and merged in the cauldron of its fiscal, economic and finally demographic

crisis; with this dream of the idealists of yore being suitably lubricated by

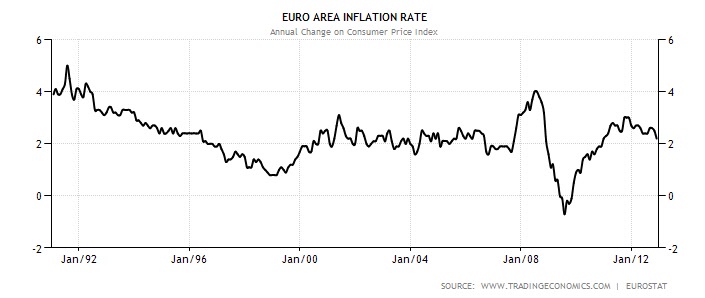

the ECB. In this pursuit, it is being helped by falling inflation (2.2% in

November, down from 2.5% in October; last year was around 3 percent)

Moreover, the

year-on-year Euro Area industrial production in October also fell by 3.6%

(seasonally adjusted) – calling for further creating/printing of new Euros.

While the ECB still remains more cautious and conservative than the Fed, it

will have to step in even more given the reality of at-best zero-growth-rate

economies. The election of Hollande’s socialist party in France has played out

as expected – discouraging entrepreneurs, and strengthening government unions.

Moreover, the resignation of the reformist, technocratic Prime Minister of

Italy, Mario Monti, has put a question mark on another too-big-to-fail European

nation. While a Greece and Portugal can be “bought off” for now, an Italy or

France or Spain faltering seriously will be the end of the Euro project, which

would not necessarily be cataclysmic if managed well (a big “if” that).

China – falling inflation point to

monetary easing here too

In November

2012, the Chinese consumer price index (CPI) went up by 2.0 percent

year-on-year. The food prices went up by 3.0 percent, while the non-food prices

increased by 1.6 percent. In the third quarter of 2012, Chinese GDP grew by 7.4

% year on year and almost 9 % annualized seasonally adjusted quarter on

quarter. Therefore, while the annual expansion was one of the slowest since

2009, the quarterly change has shown improvement. On the trade front, like the

growth front, also we have mixed signals – only inflation seems to be a

relatively clearly indicator.

Structurally,

the Chinese growth is chugging along well despite no new major government stimulus

and still weak global demand, which is a testament to the diligence of the

Chinese people. The property markets of free market havens, Hong Kong and

Singapore, have had to take unprecedented protectionist/stamp duty measures to

thwart rich Chinese buyers (so as to prevent bubbles) in the wake of Western

monetary easing washing up on Asian shares rather quickly. Yet, China has not

exactly turned corners. Also, the Chinese national bond regulator has temporarily stopped approving debt sales

by governments below provincial level, thereby sending out a signal,

however credible, against implicit federal guarantees and thereby strengthening

the stimulus reservoir strength at the national level in some future

contingency (sub-national Chinese insolvency was causing some prominent

investors a lot of jitters).

It seems that

while the Americans are expanding the monetary base, but not subsequent layers

of credit, the Chinese are to some extent accelerating investment credit

outflows through their banking systems while not necessarily focusing on the

monetary base per se. This latter plan of action is of course only possible in

more tightly controlled banking systems, and has its own downsides in

efficiency and corruption. The Chinese economic expert and “bear”, Dr. Michael

Pettis, remains pessimistic about China in the mid term noting that “of the

dozens of developing economies that have experienced investment-driven growth

miracles in the past 100 years, the only ones that have managed the transition

to developed country status are South Korea, Taiwan, and maybe Chile” and hence

China will have to face a painful transition from its mercantilist, centralized

model to a more market-finance based one.

Probable impact of all this on India -

short-term equity bullishness

Besides some

domestic reforms (FDI policy in retail being passed in both houses of the

parliament), the Indian markets have been buoyant for these external factors as

well, and this could be the beginning of another mini-rally with higher tops

and higher lows. But, India’s monetary policy remains cautious and fiscal

policies remain reckless – slowing growth have resulted in advance tax receipts

growing by just (annualized) 10.4% in December so far (collections grew even

slowly at 7.5% on year between April and December, with the nominal growth rate

all along being just shy of 15%, 6 percent growth plus 9 percent inflation

roughly speaking).

In a battle

of wills between politicians and central bankers, the latter are more likely to

blink first. Tax breaks to invest in Indian bonds were declared earlier to

attract foreign and/or privative investments, and this is already showing

results. Ennore Port in Tamil Nadu is

already issuing bonds worth Rs. 1000 cr within this scheme. On the other hand, there have been many

“deforms” as well. Life Insurance Corporation (LIC) and now even the Employees’

Provident Fund Organization (EPFO) are being raided by the Government of India

(GoI) for its fiscal purposes, destroying more necessary firewalls between various

quasi-arms of the state. The Food bill, like NREGA, is going to be high on

redistributive expenditure and low on allocative efficiency – there is no plan

to currently use private retail outlets (existing ration shops would be used)

Indian

foreign reserves have been stable at around 300 billion USD for many years even

as the economy continued to grow, showing that any dramatic appreciation of the

rupee is very improbable now. In fact, our overall macro policies are fairly

balanced with remittances providing a solid support that needs to be always

remembered given the sticker shock of our trade deficit numbers. India is the

only huge nation with a demographic surplus for the next few decades, and

emigration should be an “export” for our accounting purposes, just like “gold

purchases” need to be considered at least partially as investments. With rating

agencies likely to be even more involved because of the government’s gradual

and further opening up to foreign financial capital, invariably a fiscal-political

balance will also be found. The long term growth story of the capitalist

democracy of India is intact, despite the hysterical headlines every now and

then.

*A special contribution by Harsh Gupta....Economist from Dartmouth University

Best Regards

Paras Bothra

paras.bothra@ymail.com

+919831070777

.bmp)